Download Market Comments PDF Here

Transition Underway

With the stock market hitting new highs on January 26, 2018, the majority of investors tended to think that the favorable trend would continue virtually uninterrupted like it had for the past 16 months. But lo and behold, volatility came roaring in as the overall market generally ended lower for the first time in 10 quarters. The 10% drop in February (the first of that magnitude in two years) was a “wake-up” call signaling that the bull market was getting tired and has now entered a transition phase.

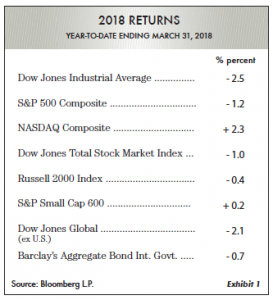

Exhibit 1 shows returns of major market averages for the first quarter of the new year through March 31, 2018.

In our January 2018 Market Comments we mentioned that major market averages had not fluctuated more than 3% for all of 2017. Performance during the first quarter of this year changed that, as the Dow Jones Industrial Average varied 12% (over 3,000 points from high to low).

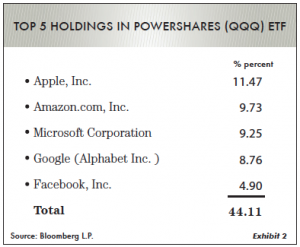

Why so much volatility? In our opinion, the advent of Exchange Traded Funds (ETFs) and Index Funds collectively are largely the cause. For example, the ETF PowerShares (QQQ) is designed to track the NASDAQ 100 Index. Look closely at Exhibit 2 showing the Top 5 Holdings in that ETF. In effect, there is very little diversification because concentration is so high in just a few stocks. Most other ETFs are in a similar situation. So when selling occurs within these issues, it causes quick damage to the (QQQ) ETF.

The ‘New’ but Different Federal Reserve

The difference between the make-up of the 2017

Federal Reserve Board and the 2018 board is quite eye-opening. For example, Exhibit 3 shows the comparison from last year’s and this year’s board members. Just think … it has taken a measly six months to increase the U.S. government debt an additional trillion dollars! Then on top of that, the President and Congress just signed a new $1.3 trillion spending bill. Total private and public debt in the U.S. is currently reported to be approximately $69.8 trillion. If the Federal Reserve raises interest rates to any degree, we will be right back in a recession. This doesn’t even count all the corporate debt that has t be repriced. So the current tough stance by the Federal Reserve Board to continually raise interest rates seems destined to fail. Interestingly, this present

Fed policy appears similar to 1981–82 when Paul Volcker, then Federal Reserve Chairman, continually raised rates in an attempt to control inflation. That strategy contributed to a severe recession. Currently the 10-year U.S. Treasury yield is at the same level as it was in January 2016. This suggests that the bond market is calling Chairman Powell’s bluff!

Over the past year, Oxbow has consistently maintained historically higher than normal cash reserves. A question posed to our portfolio managers from time to time: Why do you hold 20% or more cash in equity oriented portfolios? The first reason for this is simple: We can’t find any attractive names that presently look undervalued. Second, if markets are near all-time highs and a transition is underway, we need to have some liquidity to take advantage of lower prices should they occur. Now the “new” board consists of more aggressive, “hawkish” people who want to raise interest rates—and only a few moderates. The majority of board members have openly expressed that they don’t worry too much about the stock market. They say they’re here to serve as part of an independent Federal Reserve Board! Really? … Let’s see what happens when a prolonged negative stock market environment develops and how much resolve the board has then. To date, these so called “policymakers” have fought only one debt bubble after another. Let’s look at the present size of the public U.S. debt picture as shown in Exhibit 4.

Just think … it has taken a measly six months to increase the U.S. government debt an additional trillion dollars! Then on top of that, the President and Congress just signed a new $1.3 trillion spending bill. Total private and public debt in the U.S. is currently reported to be approximately $69.8 trillion. If the Federal

Reserve raises interest rates to any degree, we will be right back in a recession. This doesn’tveven count all the corporate debt that has to be repriced. So the current tough stance by the Federal Reserve Board to continually raise interest rates seems destined to fail. Interestingly, this present Fed policy appears similar to 1981–82 when Paul Volcker, then Federal Reserve Chairman, continually raised rates in an attempt to control inflation.

That strategy contributed to a severe recession. Currently the 10-year U.S. Treasury yield is at the same level as it was in January 2016. This suggests that the bond market is calling Chairman Powell’s bluff! Over the past year, Oxbow has consistently maintained historically higher than normal cash reserves. A question posed to our portfolio managers from time to time: Why do you hold 20% or more cash in equity oriented portfolios? The first reason for this is simple: We can’t find any attractive names that presently look undervalued. Second, if markets are nearall-time highs and a transition is underway, we need to have some liquidity to take advantage of lower prices should they occur.

Why is this important? Notice Exhibit 5 shows the long climb back that is needed just to break even when fully exposed to market downturns.

Even a small percentage of liquidity is important. Our income portfolios have been fading the transition of the Federal Reserve raising short-term rates. As an example, the yield on the 1-year U.S. Treasury has been trending up for some time. Two years ago, the yield was 0.5% and now is 2.05%. What we at Oxbow have been doing is waiting it out as a defensive measure. We are now beginning to buy some 1-year Treasuries and CDs, all of which are part of our conservative investment strategy during this transition period. We are taking what we feel is the best course to follow. Preservation of capital is always important, especially when prices are sky-high. While we are participating in the fixed income and equity markets, it is just not at the 100% level.

Market in Transition

Currently there are a tremendous number of mixed signals facing financial markets. The main message, however, is clear … Things Are Changing. The time to buy into market dips appears to be over and selling on up days seems more appropriate.

The bloom is wilting from the majority of tech stocks, and confusion is the feeling of the day.

The dominant complexion of the overall

market is shifting. With big volatility, most market pundits are still saying, Don’t worry; higher prices lie ahead. Going back to January 26, 2018, almost everyone was living high on the stock market’s future. How rapidly the air has come out! This is not the time, in Oxbow’s view, to try to be an investing hero. Most important, measure carefully what you own and why you own it. In short, we feel that now is a prudent time to maintain some liquidity. We intend to do this until we find more appealing true values in both fixed income and equities.

Oxbow Advisor – Ted Oakley – Bob Walsh