Download Market Comments Document Here

Confusing Times

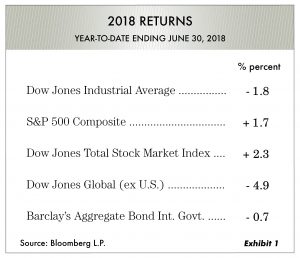

The performance of financial markets could not have been more mixed than they were in the second quarter of 2018. For example, by mid-year the U.S. stock market was positive, other than the blue chip Dow Jones Industrial Average which slipped -1.8%. Meanwhile, returns for almost every foreign stock market were down for the same time period. Results of major U.S. stock market averages for the period ending June 30, 2018, are shown in Exhibit 1, while returns for world markets are shown in Exhibit 2.

There appear to be a number of current economic and political variables that are influencing investing and confusing the vast majority of investors. The “synchronized global growth” thesis that existed for most of the past two years has withered. In addition, we have, in our opinion, a Federal Reserve board that is getting far too aggressive on raising interest rates. Also, there’s an administration in Washington that is throwing tariffs around like they are penalty flags on a football field. Meanwhile, mortgage rates are rising, inflation has moved higher, and pundits on both sides are stating their case. It’s no wonder with all these mixed signals that investors are acting like deer in headlights-since their bonds are down and the bulk of their stocks aren’t doing anything.

Let’s Examine the Tariff Situation

The administration has decided to create a trade war with Mexico, Canada, China and Europe. China in particular probably has bigger negative consequences for the stock market than for the economy.

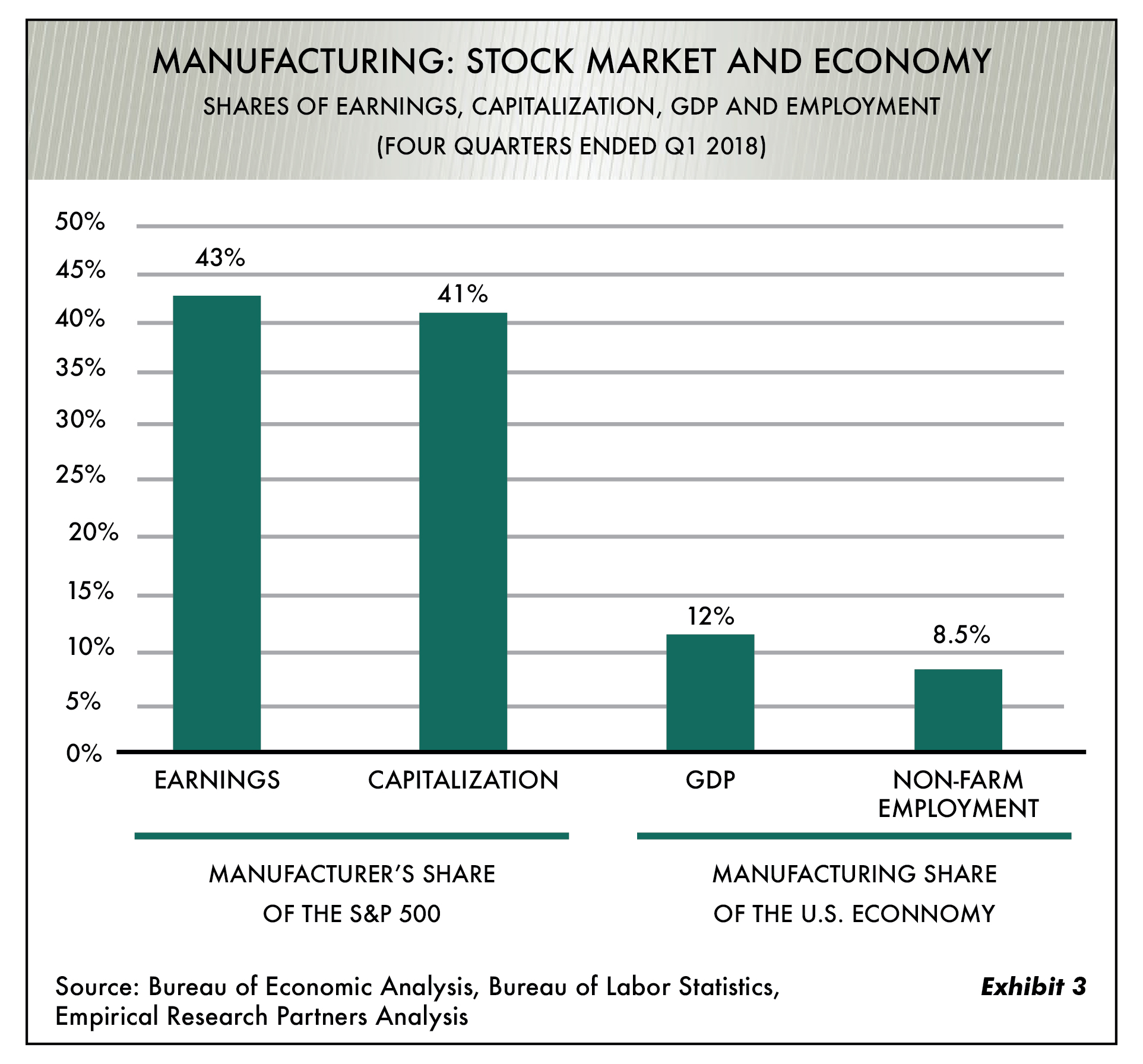

As shown in Exhibit 3 our friends at Empirical Research Partners produced some interesting data illustrating how big of a percentage manufacturing accounts for earnings in the S&P 500, and how little its share represents the total U.S. economy.

Think about this fact for a moment. Manufacturers account for only 12% of GDP and only 8.5% of non-farm employment. Here’s the problem: They account for 43% of the earnings in the S&P 500. The tariffs primarily affect the supply chains of U.S. manufacturers because half of Chinese exports to the U.S. are high-tech products. The suppliers of most of the Chinese finished goods are U.S. affiliates. When you inflict pain on the China market, you do the same to the U.S. stock market.

The Fed

The Federal Reserve still can’t seem to relate to Main Street, as the Fed unfortunately appear to reside too high in their ivory towers. Now, most key senior people in the financial system agree that the U.S. economy is enjoying abundant growth, and that leads to justifying higher interest rates. They seem to see no end to rate increases in 2018 and 2019. With most world stock and bond markets in disarray, the Fed is almost blind to everything else as they’re determined to show how committed they are to raising rates.

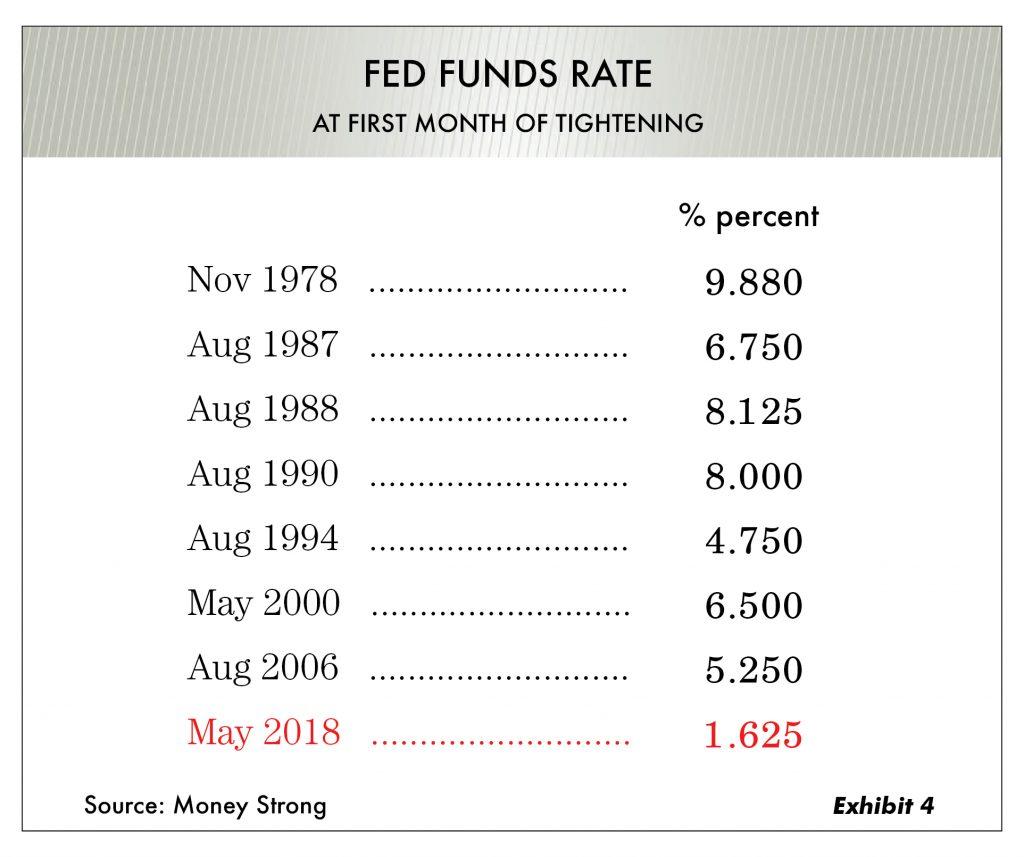

Coping with the level of interest rates seems to be the biggest problem for the Federal Reserve. It gets down to percentage increases, not absolute increases. For example, Exhibit 4 shows the Fed Funds rate that existed at the first month of tightening. What this says is that the risk of tightening is very high because it started from such a low 1.625% level.

Between the new tax law, which is negative for nearly all individuals, and next year’s trillion-dollar deficit, things don’t appear to bode well for a future robust economy. Considering this, it’s hard to understand why Fed Chairman Jerome Powell is saying, “The economy is doing very well. “ With commodity prices down so far this year and employee wages flat, we at Oxbow do not see inflation numbers moving much higher. The surprise over the next 12-18 months could be that interest rates actually trend lower.

Index Funds and Robo Investing

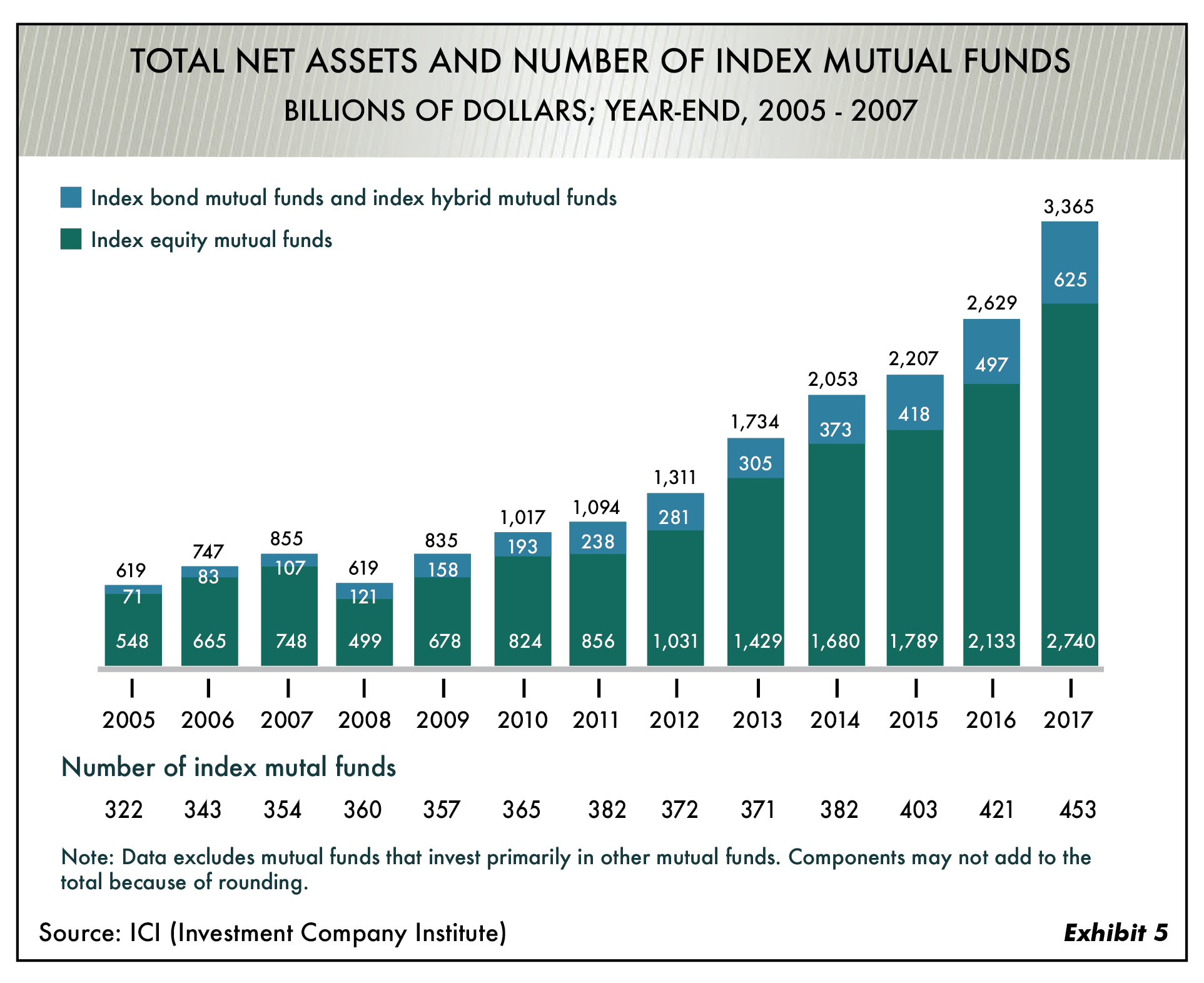

Index investing is simply following exactly what the index does. Robo investing is akin to robotic investing with minimal human input, merely using software to make decisions. John Bogle, the founder of Vanguard, recommends selling all individual stocks and investing in low-cost index funds. This approach has worked well for the past six years because there have been zero market wrecks. Notice Exhibit 5 showing the significant growth of index fund assets since 2005.

Much of what good investment managers do centers around helping people overcome their own bad emotional behavior. Indexing is based on buying the whole stock market and then doing nothing. The problem is “doing nothing.” As an example, if the overall stock market were to fall by -20% and your industry wasn’t doing so well, the investor would still say “Don’t worry about buying and holding an index or robo fund.”

Then, months go by and the market is down -30% and your spouse says, “I’m worried about this; we need to stop and think.” Six to eight months later, the market is now down -40% and all of a sudden, the investor looks backwards and feels reckless. They are also in a state of emotional weakness, so they sell out. This ingredient is the missing element of investing in index and robo funds.

At this point, a good professional advisor can help keep investors where they should be. Results over the past six years, using the index approach, has been favorable, but it likely won’t last forever. Indexers fail to realize this. It will be a tough time at some point because everyone around you is losing as their emotions also take over. Maybe you think you can resist these forces, but so does everyone else. In point of actual fact, the dominant determinant of long-term investment outcome is based on investor behavior. Without behavioral counsel (for which there is a cost), human nature will fail most investors.

The First Six Months of 2018

At Oxbow, we feel we’re doing a good job of steering our investors through a most difficult and confusing time in the stock market. In our April 2018 Market Comments we labeled 2018 likely to be a year of transition where returns are noticeably lower than they were for the bulk of the nine-year bull market that began in early 2009. The investment environment is full of mixed signals that suggest the bull market is well along in its maturity stage and is tired. Our current fixed-income portfolios have outperformed, and our equity portfolios have performed in line with the overall stock market despite our decision to hold higher cash reserves. This conservative strategy has helped to more effectively manage risk.

Looking Ahead

In our opinion, the next two quarters of this year will be important for investors. During this time, we should start to see if the economy is really coming alive or if it had just one burst of energy earlier in 2018. For now, we intend to keep our investment strategy defensive and continue to seek out opportunities.

We wish you all the best during these summer months.

Ted Oakley

Bob Walsh

“Worrying is like a rocking chair. It gives you something to do, but it doesn’t get you anywhere.” -VAN WILDER